A 2026 Market Analysis of Deployment Readiness, Economic Viability, and What Investors Should Actually Measure

The humanoid robotics sector has entered a serious phase.

Capital is flowing. Industrial pilots are public. Manufacturing ambitions are being announced in quarterly earnings calls. Platforms from the United States, China, and Europe can now walk, lift, grasp, and perform increasingly complex task sequences.

Yet beneath the acceleration lies a quieter question:

How many of these systems are actually working consistently, economically, and at scale?

As The Economist noted in its recent coverage of embodied AI, the real challenge for humanoids is no longer motion, but usefulness. The publication observed that building robots that move convincingly is no longer the frontier; building robots that “generate economic value in messy real-world environments” is.

(Source: The Economist, “The Rise of Humanoid Robots,” Science & Technology section)

That distinction is subtle but decisive. A robot that moves convincingly is not necessarily a robot that can sustain value inside a real workflow. That is where this market will separate.

Deployment Is Where Friction Begins

Locomotion has advanced quickly. Balance control, dynamic gait, and upper-body dexterity are no longer experimental achievements.

Deployment, however, introduces different constraints.

In warehouse pilots and industrial trials, the recurring friction points are rarely dramatic failures. They are cumulative degradations:

- inconsistent manipulation reliability

- intervention frequency higher than modeled

- slow recovery from minor errors

- maintenance cycles interrupting productivity

Research from RAND on autonomy systems repeatedly emphasizes that failures in complex robotic systems often arise not from a single subsystem breakdown, but from integration friction between perception, control, environment, and human workflow. That pattern is visible in humanoids today.

The industry is transitioning from engineering milestones to operational metrics.

This gap between technical capability and real-world productivity has been described by Andreessen Horowitz as the “physical AI deployment gap”. The distance between systems that function in controlled environments and those that deliver consistent economic value in operational settings. In their analysis, a16z argues that robotics and embodied AI companies often underestimate the complexity of deployment, integration, and sustained reliability once systems leave the lab.

(Source: Andreessen Horowitz, “The Physical AI Deployment Gap”)

Kinisi and Tesla: Two Paths to the Same Constraint

Kinisi Robotics has adopted a wheeled-base humanoid architecture. The rationale is straightforward: reduce fall risk, simplify navigation, and accelerate near-term deployment inside structured environments like warehouses.

Tesla’s Optimus program is pursuing a fully bipedal general-purpose humanoid, supported by internal AI and manufacturing scale. Elon Musk has stated publicly that Optimus could eventually become “Tesla’s most valuable product,” emphasizing mass production and long-term deployment ambitions.

(Source: Tesla AI Day presentations; coverage by The Verge and Wall Street Journal)

But both ultimately face the same constraint:

Cost per productive hour. For investors, the relevant questions are not stride length or lift capacity. They are:

- How many hours has the system completed without intervention?

- What is the supervision ratio?

- What happens after the 1,000th repetition of a task?

The humanoid is not competing against other humanoids alone. It is competing against forklifts, conveyors, cobots, and human labor with flexible scheduling.

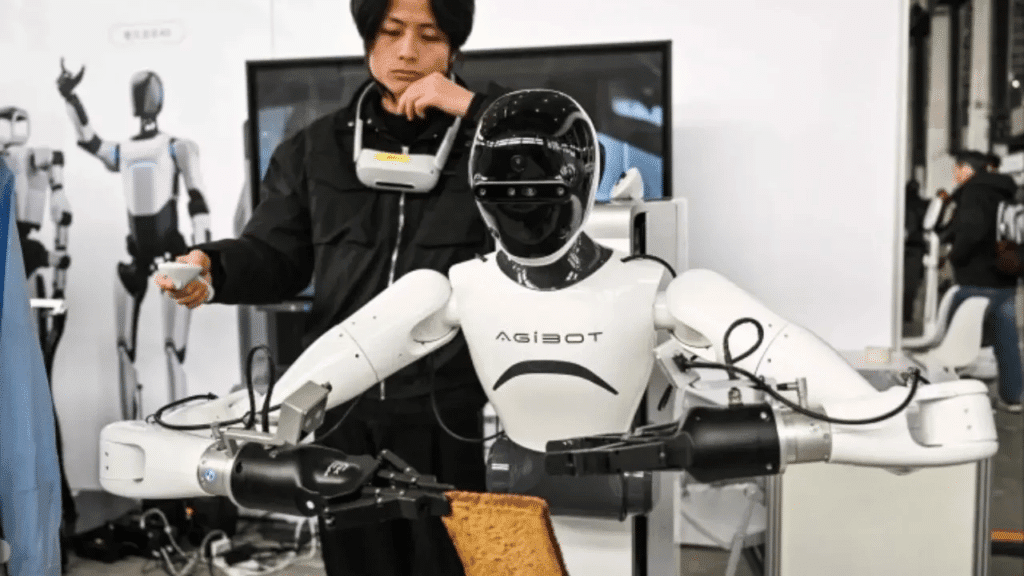

AGIBOT and Unitree: Scale Narratives and Cost Pressure

AGIBOT has emphasized manufacturing scale and an embodied AI ecosystem approach. Unitree has entered the humanoid market with aggressive pricing and rapid hardware iteration.

Both strategies are rational.

But scale claims must translate into measurable productivity, not shipment volume. Affordability must coexist with sustained reliability under load.

Across conference disclosures and public pilot reports, a recurring theme emerges: locomotion is often reliable earlier than manipulation under real variability.

As roboticist Rodney Brooks, co-founder of iRobot and former MIT CSAIL director, has written:

“The real world is messy, and robots that haven’t been tested in that mess will fail in surprising ways.”

(Source: Rodney Brooks, IEEE Spectrum / Robots, AI, and the Reality Gap)

Getting a robot to lift a standardized object once is engineering. Getting it to repeat that task thousands of times with low variance is operations. That difference is where margin lives.

Boston Dynamics: Discipline Over Spectacle

Boston Dynamics’ transition to an electric Atlas platform signals clear industrial intent. The company’s messaging has shifted from athletic performance to practical task framing.

That shift is meaningful.

High-performance motion generates attention. Predictable industrial behavior generates revenue.

The primary constraint for high-engineering platforms is not capability, but economics. Advanced actuation, control systems, and safety engineering increase cost. Cost narrows early market adoption.

Mentee Robotics and Integration Complexity

Mentee Robotics’ acquisition by Mobileye signaled confidence in embodied AI as an extension of perception and autonomy stacks. The integration opportunity is substantial. So is the complexity.

Large organizations can provide capital, infrastructure, and AI expertise. They can also introduce process layers that slow real-world iteration. In robotics, iteration speed in operational environments is often more important than laboratory acceleration.

Deployment cadence matters more than press cadence.

1X and the Consumer Threshold

1X Technologies is pursuing humanoids in home and service environments. The domestic domain is structurally more complex than industrial settings. Warehouses can be optimized. Homes cannot.

As The Economist has argued in broader automation coverage, consumer robotics succeeds when it becomes invisible, not when it is impressive. In domestic environments, failure tolerance is low and trust is fragile.

The economic equation in homes is also different. Productivity metrics are harder to define. Liability thresholds are higher. The consumer humanoid market will move slower than the industrial one.

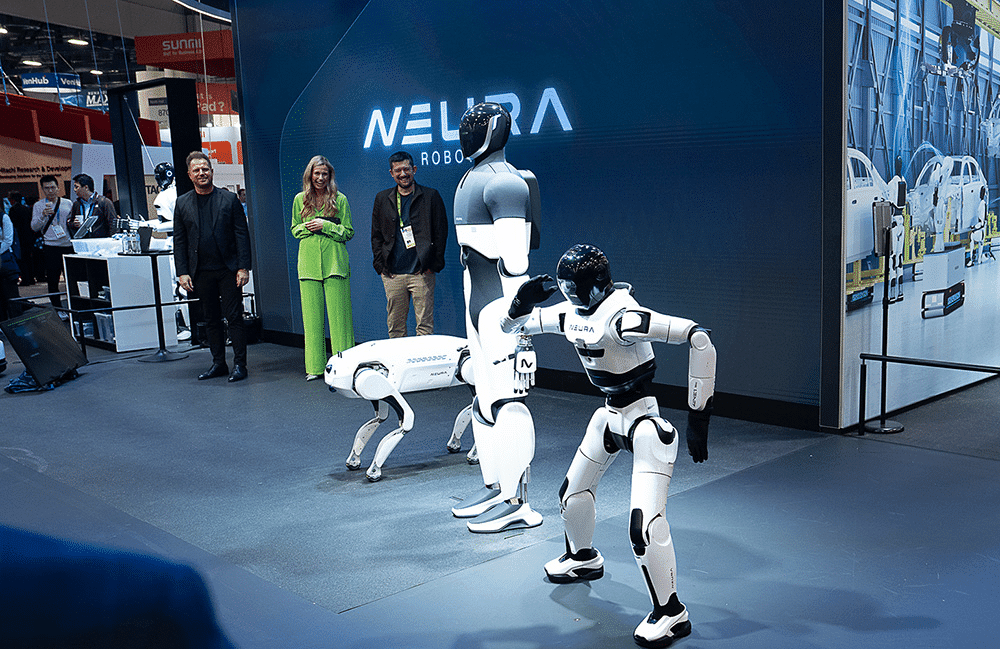

NEURA Robotics and the European Position

NEURA Robotics emphasizes safety, compliance, and European industrial integration. In a crowded global market, regulatory alignment can become a wedge.

But a wedge must be concrete, as Philipp Raasch shares on his latest post

Cities such as Turin, Wolfsburg, and regions like Hauts-de-France are not abstract industrial examples, they are home to deeply established automotive production ecosystems. These factories are highly automated, yet still rely on human labor for repetitive, physically demanding, and adaptation-heavy tasks. Humanoids, if they reach sufficient reliability, could integrate into these environments not as replacements for automation, but as flexible extensions of it.

The humanoid companies that survive saturation will be those anchored in specific verticals: automotive assembly, warehouse logistics, heavy repetitive handling, or narrowly defined service tasks. Strategic ambiguity is expensive in capital-intensive robotics.

UAX Diagnosis: What This Market Is Actually Testing

From our perspective, the humanoid sector is not currently testing engineering creativity. It is testing operational discipline.

The decisive variables over the next 12–18 months will likely be:

- Supervision ratio reduction

- Mean time between human intervention

- Maintenance simplification

- Fleet management infrastructure

- Learning velocity across sites

- Team work

We do not expect broad consumer deployment in the next year. Industrial pilots will expand cautiously. The winners will not necessarily be the most visible companies today.

They will be the ones quietly accumulating task hours.

The next year will likely bring:

- More factory pilots

- Limited but growing warehouse integration

- Strong capital consolidation

- A narrowing field as economic reality filters ambition

Humanoids will not disappear. But the market will become less tolerant of narrative without throughput.

The Next 12 Months: What to Watch

Investors should monitor:

- Public disclosure of productive hours, not just pilot announcements

- Evidence of reduced teleoperation reliance

- Clear ROI statements from integrators or end customers

- Maintenance cost transparency

- Safety incident reporting frameworks

Capital will continue to flow. But capital will begin asking harder questions.

The companies that can answer them with data rather then demos, will shape the next stage of this market. UAX conducts structured technical diligence for robotics, autonomy, and humanoid systems, helping investors and operators evaluate deployment readiness before capital scales.

Conclusion

The humanoid race is not about proving that a robot can walk.

It is about proving that it can work – consistently, safely, and economically.

In 2026, spectacle still attracts attention. But sustained productivity will determine survival.

In robotics, uninterrupted shifts are worth more than applause.